Find the best Medicare option for your life

Educating yourself today can benefit you greatly in the future

If you or a loved one is nearing retirement, now is the time to start researching the best option for insurance. Medicare is a federal insurance program for people over 65 regardless of income, medical history or health status.

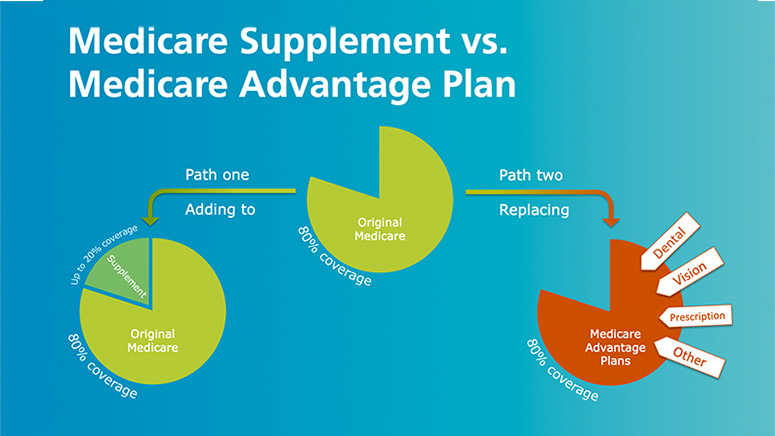

There are two main paths to choose from:

Medicare Supplement vs. Medicare Advantage Plan

Path 1 – Medicare Supplement (also known as Medigap) is a supplement to traditional Medicare that fills in the gaps not covered by traditional Medicare. There are a variety of Medicare Supplement plans available depending on your needs and budget. Each one has different premium and deductible amounts

Path 2 – Medicare Advantage (also known as Medicare Part C) is private insurance that replaces traditional Medicare. When you enroll in a Medicare Advantage plan, you are giving up traditional Medicare and replacing it with the Medicare Advantage plan. The Medicare Advantage company is acting as a subcontractor to Medicare. Medicare requires these Medicare Advantage plans to offer the equivalent to what you would get from traditional Medicare which equates to 80% of coverage. These plans, like traditional Medicare, typically cover around 80% of health care needs. They often come with little to no premium but may leave participants responsible for as much as $8,850 in out-of-pocket expenses in 2024. Also, keep in mind that even with a $0 premium Medicare Advantage plan, you will be required to pay the Medicare Part B premium.

When choosing the path that’s best for you, keep the following key considerations in mind:

Costs and your budget: Make sure you compare not only the premiums – but also factor in coinsurance, copays, deductibles and out-of-network expenses and limits for a more complete picture of each option’s costs.

Medicare Supplement plans often have higher premiums but lower out-of-pocket expenses. This is a good option if you want predictability in your health care expenses that you can budget for and lower out-of-pocket expenses.

If you choose a low- or $0-premium Medicare Advantage plan, you likely will need to plan ahead and budget for higher out-of-pocket expenses. $8,850 is the Medicare Advantage deductible for 2024. This amount changes every year.

“You could end up paying more out of pocket. While the low monthly premiums of Medicare Advantage plans may be alluring, you risk paying more in the long run in the form of co-payments, deductibles, and other OOP costs. If you develop a serious illness or chronic condition, these costs can pile up quickly (and exceed what you’d pay with Original Medicare).” – National Council on Aging (https://www.ncoa.org/article/what-is-the-difference-between-medicare-advantage-and-medigap)

“[Medicare Supplement] can help make your Out-of-pocket costs more predictable and affordable: Since Medigap (Medicare Supplement) provides reimbursement for some or all of your Medicare Part A & Part B copayments and deductibles (depending on your plan), you don’t have to worry about cost every time you visit a doctor or hospital. Most Medigap plans cover the Medicare Part A hospital deductible, which is [$1,632 in 2024]. Should you experience a health emergency or extended hospital stay, Medigap coverage can save you a significant sum.” – National Council on Aging (https://www.ncoa.org/article/what-is-the-difference-between-medicare-advantage-and-medigap)

Coverage needs: What do your health needs look like now? What will they look like in five years? 10 years? 20 years? Future health care needs are hard to predict. Keep in mind that as we age, our health – and by extension our health care needs – change. It is important to take the long view and choose a plan that will provide the coverage you need when the unexpected happens. The plan you choose could help cover frequent doctor visits, lab tests, hospital stays, rehabilitation and even hospice care, if needed.

Medicare Advantage plans replace traditional Medicare and only cover around 80% of health care costs.

Medicare Supplement plans supplement Medicare, and many plans cover nearly 100% of health care costs.

Choice of doctors and hospitals is a key difference between selecting traditional Medicare with a Medicare Supplement plan vs. a Medicare Advantage plan.

With Medicare Supplement plans, you can choose any provider or hospital that accepts Medicare across the U.S., which most do. In fact, some plans, including most Everence Medicare Supplement plans, also offer foreign travel emergency coverage. Also, keep in mind that if you qualify for rehabilitation after a hospital stay, you can go to any rehabilitation facility that accepts Medicare.

With Medicare Advantage, you must choose from the plan’s network of providers, hospitals and rehabilitation facilities. Review the list for your local and preferred providers and what the plan covers beyond your local region. In most cases, your expenses rise dramatically if you choose an out-of-network provider.

While some Medicare Advantage plans have in-network providers beyond your local area, you’ll want to investigate the depth and geographical scope of any Medicare Advantage plan’s network if you travel frequently or live part of the year in another area.

“You may be restricted in what providers you see: Original Medicare allows you to see any health care provider that accepts Medicare. However, Medicare Advantage plans typically don’t give you that freedom of choice. Many of these private plans have a designated network of providers restricted to a member’s geographic area. Except for emergencies, some plans may not cover care outside of their defined service area—or they may impose higher cost sharing or prior authorization rules for out-of-network care.

This limited access means you might not be able to see the best (or your preferred) providers when you have a need. It may also be challenging to find providers if you live in a rural area.

What's more, with Medicare Advantage, you may have to get a referral from your primary care provider if you want to see a specialist. This extra visit translates into extra time and expense.” – National Council on Aging (https://www.ncoa.org/article/what-is-the-difference-between-medicare-advantage-and-medigap)

Guaranteed issue: When you sign up for traditional Medicare and a Supplement plan or a Medicare Advantage plan upon retirement, you cannot be denied coverage.

With Medicare Advantage, you have the option to enroll in a plan during open enrollment each year.

With traditional Medicare and Medicare Supplement plans, you can enroll without a medical assessment, also known as underwriting, when you first become eligible – either by age or employment status beyond age 65. Then, you have a six-month period after that in which you can make changes.

If you choose Medicare Advantage upon retirement, you will not be able to switch to a Medicare Supplement plan without successfully passing a health assessment (underwriting). It is not easy to switch from Medicare Advantage to Medicare Supplement if you need care due to a medical event or new diagnosis.

Prior Authorization: Traditional Medicare does not require prior authorization for health care services, with only a few exceptions such as durable medical equipment or rehabilitation services.

Medicare Advantage insurers are private companies contracting with the federal government to provide Medicare benefits. As private companies, they can choose to impose prior authorization requirements to prevent patients from receiving treatment or services they deem unnecessary. Studies done by bipartisan research organizations and the federal government in recent years show a surge in inappropriate denials of services to patients and denial of payments to health providers by these private insurance companies.

One man (age 76) has a Medicare Advantage plan, and he said it was great until he developed melanoma. After his diagnosis, he had a hard time finding the care he needed. He wanted to switch to traditional Medicare with a supplement plan, but he wasn’t approved because of his preexisting condition. Read his story in the article below.

“Older Americans say they feel trapped in Medicare Advantage plans” - Kaiser Health News (https://www.wmra.org/2024-01-03/older-americans-say-they-feel-trapped-in-medicare-advantage-plans)

“MAOs (Medicare Advantage Organizations) denied prior authorization and payment requests that met Medicare coverage rules by:

- using MAO clinical criteria that are not contained in Medicare coverage rules;

- requesting unnecessary documentation; and

- making manual review errors and system errors.” – US Dept. of Health and Human Services Office of Inspector General (https://oig.hhs.gov/oei/reports/OEI-09-18-00260.pdf)